Every spring, millions of Canadians file their taxes — and every spring, millions of Canadians have only a vague idea of how the numbers actually add up. If you've ever looked at a raise and wondered "how much of this do I actually keep?", or heard someone say "I'm in the top tax bracket" with a kind of resigned dread, this guide is for you.

The good news: Canada's tax system is far more logical than it seems. Once you grasp two core ideas — marginal rates and average rates — the rest clicks into place. Let's break it down.

How Canadian Income Tax Actually Works

Canada uses a progressive tax system. This means that as you earn more, you pay a higher percentage — but only on the income within each specific range, called a bracket.

Think of it like filling buckets. The first bucket holds your lowest earnings. It fills at a low tax rate. Once it overflows, the excess spills into the next bucket, which is taxed at a slightly higher rate — and so on. You never pay the higher rate on all your income, only on the portion that falls into that bucket.

Key Insight You are always taxed on a combination of federal and provincial rates. Both levels of government take a slice. This guide covers both.

You also have a Basic Personal Amount (BPA) — a credit that means your first ~$16,129 of income (federally, 2025) is effectively tax-free. Every Canadian gets this.

Marginal vs. Average Rate — The Key Distinction

This is the single most important concept in Canadian taxes, and the one most misunderstood. Let's define both clearly:

Marginal Tax Rate - 26.5%

The rate applied to your next dollar of income. This is your "top bracket." It does not apply to everything you earn — only to the slice at the top of your income stack.

Average (Effective) Tax Rate - 17.3%

Your total tax paid divided by your total income. This is what you actually give to the government. Almost always much lower than your marginal rate.

These two numbers for a $90,000 Ontario income. Notice how different they are? Your marginal rate is 26.5% but you're effectively paying only 17.3% of your total income in federal + provincial tax.

A Simple Analogy

Imagine a parking lot where the first 2 hours are $3/hr, the next 3 hours are $6/hr, and any time beyond that is $10/hr. If you park for 6 hours total, you don't pay $10 × 6 = $60. You pay (2 × $3) + (3 × $6) + (1 × $10) = $34. Your marginal rate (the last hour) is $10/hr — but your average rate is $5.67/hr.

Canadian income tax works exactly the same way.

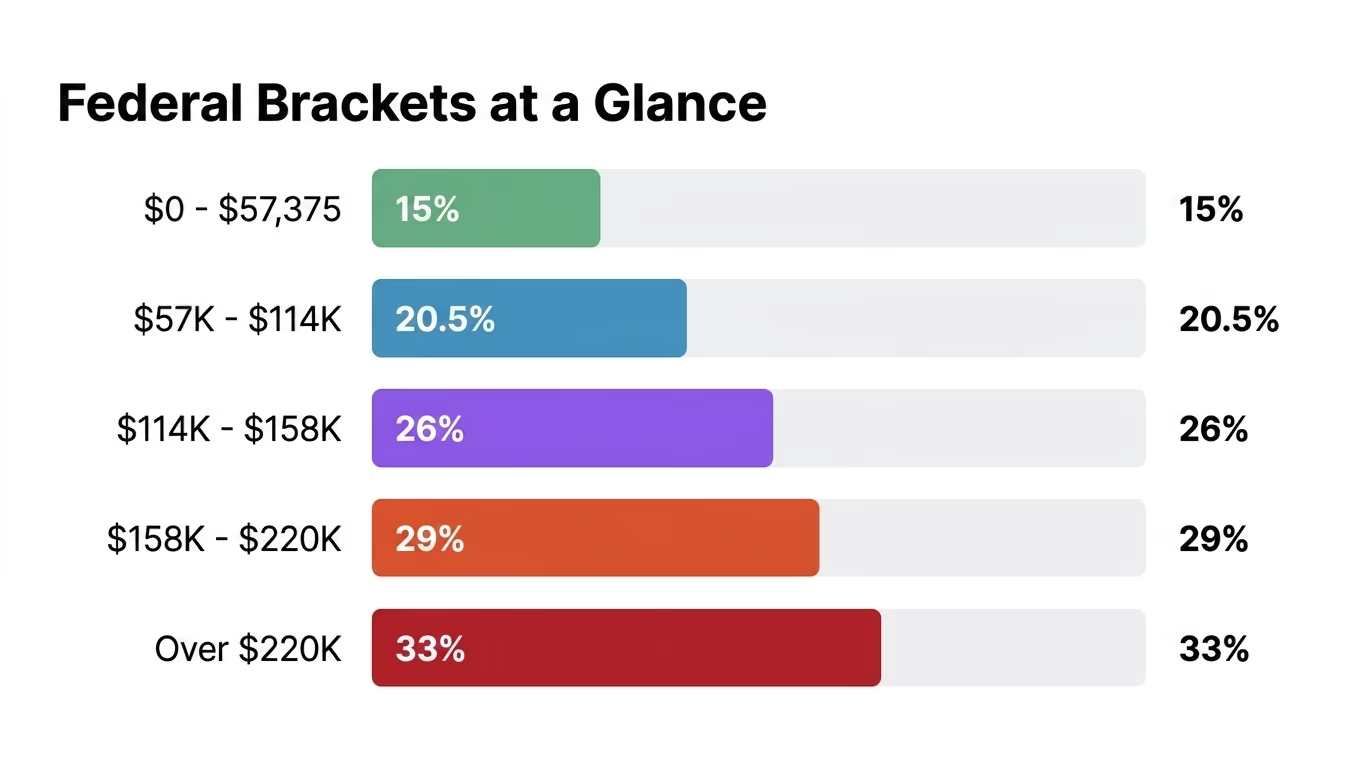

2025 Federal Tax Brackets

Here are Canada's federal income tax brackets for 2025. Remember — these apply only to the income within each range, not your total earnings.

📌 Don't forget provincial tax

Federal brackets are only half the story. Each province adds its own tax on top. Your combined marginal rate (federal + provincial) is what really matters. Use the calculator below to see your full picture.

How a $90,000 Income Moves Through the Brackets

Let's trace exactly what happens with a $90,000 salary at the federal level only (before provincial). This makes the "only the top slice" rule concrete:

Tracing $90,000 through the federal brackets

15%

First $57,375 is taxed at 15%. This fills the first bucket completely.

$8,606

20.5%

The remaining $32,625 ($90,000 – $57,375) falls in the second bracket.

$6,688

—

Total federal tax (before BPA credit of ~$2,419)

$15,294

✓

After Basic Personal Amount credit: Federal tax owed

$12,875

Your marginal federal rate is 20.5% — that's the bracket your last dollar landed in. But your average federal rate is only about 14.3% ($12,875 ÷ $90,000).

Canadian Tax Calculator 2025

Busting the Big Tax Myth

The most damaging misconception in personal finance Canada: "Getting a raise pushed me into a higher bracket, so I'll actually take home less money."

This is false. It can never happen under Canada's system.

Because only the new income is taxed at the higher rate, a raise always increases your take-home pay. If you earn an extra $1,000 and the marginal rate on that money is 43.41% (say, Ontario combined), you keep $566. You don't lose money. You gain $566.

The Rule

Under a marginal tax system, earning more money always means more money in your pocket — never less. The only thing that changes is the rate you pay on the extra amount.

How to Reduce Your Taxable Income

Understanding your bracket also reveals exactly how much value tax-sheltered accounts provide. If you're in the 43% combined bracket and you contribute $10,000 to an RRSP, you save $4,300 in taxes — immediately.

Top Ways to Lower Your Tax Bill

RRSP Contributions: Deduct from taxable income at your marginal rate. Most powerful for high earners.

TFSA Contributions: Growth inside the account is tax-free. No deduction now, but never taxed later. Ideal for all brackets.

FHSA (First Home Savings Account): Combines RRSP-like deductions with TFSA-like tax-free growth if used for a first home purchase.

Capital Gains Inclusion Rate: Only a portion of capital gains are included in taxable income — this is why investments are often taxed more favourably than employment income.

Pension Adjustments & RPP Contributions: If your employer offers a Registered Pension Plan, contributions reduce your taxable income directly.

Frequently Asked Questions

Q: What's the difference between a tax credit and a tax deduction?

A: A tax deduction (like an RRSP contribution) reduces your taxable income, so the tax savings depend on your marginal rate. A tax credit (like the Basic Personal Amount) directly reduces the taxes you owe by a fixed dollar amount, regardless of income. Credits are generally more equitable; deductions benefit higher earners more.

Q: Does Quebec work differently?

A: Yes. Quebec residents receive a federal abatement (a partial refund of federal tax) because Quebec runs its own pension plan (QPP) and parental insurance (QPIP) programs. Quebec also has its own separate provincial tax return. The calculator above includes Quebec's combined rates.

Q: What about CPP and EI contributions?

A: Canada Pension Plan (CPP) and Employment Insurance (EI) premiums are separate from income tax but reduce your net pay. For 2025, CPP deductions apply on earnings between $3,500 and ~$73,200. These aren't included in the calculator above — it focuses on income tax only. Add approximately 4.95% (CPP) and 1.66% (EI rate on insurable earnings) for a complete payroll picture.

Q: When do the brackets get updated?

A: Canada indexes tax brackets annually to inflation using the Consumer Price Index (CPI). The CRA announces updated brackets each November for the following tax year. Brackets for 2025 were indexed by approximately 4.7% from 2024 levels.

Q: I'm self-employed. Does any of this change?

A: The tax brackets are the same, but self-employed individuals pay both the employee and employer portions of CPP (9.9% on net business income up to the ceiling), which significantly increases total deductions. The upside: many business expenses are deductible, which lowers your taxable income before brackets even apply.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial, legal, or tax advice. While data is based on current 2026 Canadian regulations, individual financial situations vary. Always consult with a certified financial planner or registered tax professional before making significant financial decisions.